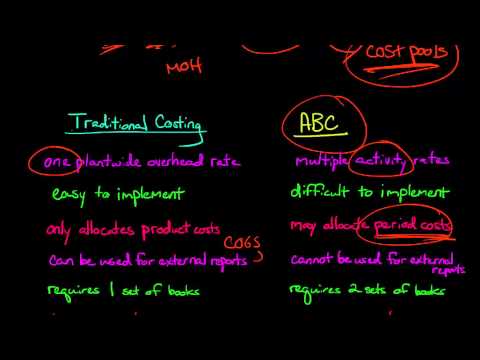

Activity based costing, often times referred to as ABC, is a method of organizing and allocating costs that are involved in a business, production, or operation of any kind. It means that you reduce over head costs by calculating exactly how much one activity costs, and allotting that much money to it. This ABC method of spending has been around since the 1980’s and has been implemented by many different businesses around the world. While cutting costs is generally a well received concept, there can be many downfalls that come along, especially with the activity based costing method of doing so.

Advantages of Activity Based Costing

1. Improves Over All Processes

During the process of implementing an activity based costing method in a business, all of the processes that are used are looked at in depth. After a short period of time, a bigger picture begins to emerge of which processes are working well and which are not.

2. Waste Is Identified

Overhead costs often include quite a few wasteful products. All of these can be identified very simply with an ABC method of cost analysis, and then removed from the business all together, or at least managed more effectively.

3. Pricing Is Better Organized

With ABC businesses are able to fully identify all the costs that are associated with producing a single unit of their product. Because of this new understanding, they are able to develop pricing strategies and marketing much more efficiently.

4. Can Be Applied To The Entire Business

It may seem that activity based costing is only effective and efficient for the production costs that are involved in a business, but all overhead costs can be reduced using this method. Everything from management, CEO’s, and entry level employees.

Disadvantages of Activity Based Costing

1. Reduction Is Not Always Possible

If the overhead costs are high for reasons such as volume, there are very limited benefits to be reaped from activity based costing. It also is not very efficient if the overhead costs of the business only represent a very small portion of the costs.

2. High Implementation Costs

ABC method of costs may not be best if the overhead waste is perceived to be relatively low. This is because it can be very costly to implement activity based costing into a business. Experts must be brought in for an extended period of time, and other measures may be necessary for the ABC to be effective.

3. Time Involved

There is a long time period that is involved in using an activity based costing method in a business. All of the production processes, employee actions, and aspects of the business have to be examined for an extended period of time in order to gain a big view on what the issues truly are.

4. Data Flaws

ABC requires many different departments and individuals to collect and input data. Even the smallest flaw in this information can damage the entire process and the outcome would be tainted. This is one of the biggest risks that are taken on when using this method.

Important Facts About Activity Based Costing